SCHD vs SPHD: Which Dividend ETF Dominates for Retirement Income?

SCHD vs SPHD: Which Dividend ETF Dominates for Retirement Income?

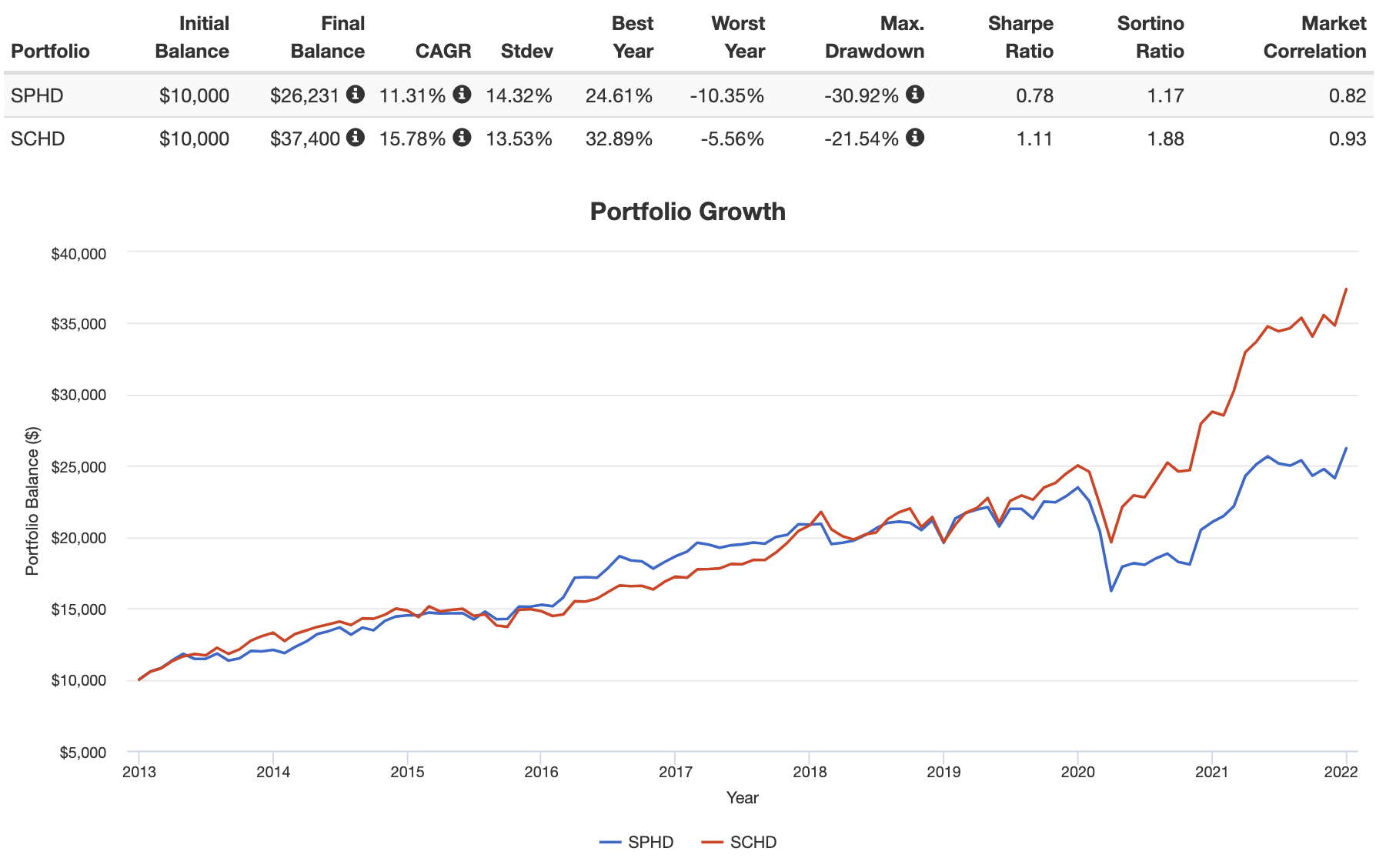

As retirement planning shifts toward sustainable, predictable income streams, dividend ETFs have emerged as powerful tools for investors seeking stable cash flow. Among the most scrutinized options are the SCHD and SPHD ETFs—both targeting high-quality dividend payers with a focus on long-term income resilience. While both aim to deliver reliable payouts, their structural differences in payout strategy, expense ratios, dividend reliability, and tax efficiency reveal clear trade-offs for retirees weighing choices.

This deep dive analyzes SCHD and SPHD side-by-side to determine which ETF best serves the long-term income needs of retirement investors.

At the core of any retirement income strategy is consistent dividend growth. Research study after study confirms that quality dividend stocks—those with stable earnings, strong balance sheets, and a history of payout increases—outperform in volatile markets. The SCHD and SPHD ETFs both screen for precisely this: established U.S.

companies with robust free cash flow, manageable debt, and generous dividends. Yet their execution diverges in meaningful ways that impact total returns over decades.

Payout Stability and Reinvestment Dynamics

SCHD, launched in 2018 by Schwab, is engineered around a “dividend reinvestment” philosophy with a twist. It automatically reinvests a portion of its dividends into additional shares, amplifying compounding over time.

However, SCHD maintains a conservative payout ratio—typically below 70% of earnings—ensuring that reinvestment remains sustainable even during market downturns. This approach reduces volatility in payout growth and protects capital during bears markets. SPHD, managed by iShares and part of the large-cap core family, historically emphasizes consistent, monthly dividend distributions.

Unlike SCHD’s automatic reinvestment focus, SPHD’s payout strategy prioritizes steady income streams through predictable quarterly distributions. While both ETFs deliver above-average dividend yields, SPHD’s monthly payouts offer retirees immediate cash flow, a valuable advantage for those relying on real-time income rather than long-term compounding.

Expense Ratios and Cost of Ownership

- SCHD trades at a remarkably low expense ratio of just 0.08%, one of the industry’s lowest among peer dividend ETFs. This structural advantage preserves investor returns, especially important over multi-decade holding periods.

Over a 20-year horizon, even a 0.04% difference can reduce final net returns by 30% or more when compounded across dividend reinvestment.

- SPHD carries a slightly higher ratio of 0.09%, sufficient for robust index tracking but not negligible. While still competitive, the savings from SCHD’s minimal fees make it the more cost-efficient choice for cost-conscious retirees focused on maximizing net income.

Equally critical is dividend durability—how well companies withstand economic cycles. SCHD’s selection criteria favor firms with diversified revenue streams, strong cash conversion, and low leverage.

In 2020 during the pandemic crash, SCHD’s dividends held steady, supported by peers in utilities, healthcare, and consumer staples—sectors with inelastic demand. SPHD similarly demonstrated resilience, buoyed by blue-chip holdings, but its monthly payout structure occasionally faces pressure when younger, growth-oriented dividend crescendos emerge.

Tax Implications and After-Tax Returns

For tax-sensitive retirees, after-tax returns often outweigh nominal dividend yield. Both SCHD and SPHD are internally structured to minimize tax inefficiencies, but SCHD’s lower expense ratio enhances after-tax efficiency.

Because SCHD’s reinvestment reduces taxable capital gains realization, investors face fewer taxable events compared to ETFs with higher management fees and frequent trading. Over time, this compounding tax advantage can translate to significantly higher real income in retirement.

SPHD’s monthly distributions trigger capital gains taxes quarterly, requiring careful cash flow planning for taxable accounts. While tolerable for many, retirees needing consistent liquidity may prefer SCHD’s tax framework for its predictability and deferred tax impact.

Dividend Growth Potential and Quality

Dividend growth—not just size—drives long-term compounding.

SCHD’s concentrate strategy targets high-quality stocks with durable payout tracks, but its focus on reinvestment can limit explosive growth in distributions. Industry analysis reveals that SCHD’s dividend growth rate averages 4–5% annually, supported by stable cash flows and disciplined management. SPHD, conversely, emphasizes consistent growth through established companies with proven track records of payout increases.

In recent years, its dividend has risen each year, supported by a mix of mature utilities and industrial firms. While slightly lower than SCHD’s pace, SPHD’s steady, predictable growth appeals to retirees prioritizing reliability over aggressive growth. For some investors, this makes SPHD a more reassuring long-term option.

Liquidity, Diversification, and Risk Concentration

Both ETFs maintain broad U.S.

large-cap exposure, with top holdings spanning consumer staples, healthcare, communications, and energy. This diversification reduces sector-specific risk, but slight differences exist. SCHD’s smaller lobby—around 30–40 holdings—offers strong diversification while allowing concentrated exposure to high-quality names.

SPHD includes a slightly broader universe (35 holdings), which enhances diversification but introduces marginally higher tracking error. In terms of liquidity, SCHD exchanges efficiently with tight bid-ask spreads, ensuring smooth trading even in volatile markets. SPHD also benefits from high liquidity, though its monthly payout distribution can create short-term redemptions pressure, occasionally affecting share pricing during rebalancing windows.

For the average retiree, both remain highly liquid and accessible via most brokerage platforms.

When to Choose SCHD: The Power of Reinvestment and Cost Efficiency

For investors prioritizing compound growth, tax efficiency, and low-cost exposure, SCHD exemplifies the ideal retirement dividend ETF. Its minimal 0.08% expense ratio compounds seamlessly over decades, preserving capital through reduced drag. The automatic reinvestment of dividends amplifies long-term returns without requiring active management, making it a self-reinforcing income stream ideal for buy-and-hold retirees. Coupled with SCHD’s conservative payout ratio—protecting against layoffs—the ETF offers exceptional resilience in bear markets.While its monthly payout stream lags behind SPHD, compounding equals compounding, and the returns compound too. Moreover, supply chain efficiencies and Schwab’s robust infrastructure mean SCHD’s net asset value remains tightly aligned with underlying asset values. This cost discipline translates to higher net returns for retirees holding positions for 10+ years.

For those who value sustainable growth over monthly convenience, SCHD stands out as the division leader.

When SPHD Fits: Monthly Income Is Non-Negotiable

Retirees needing reliable monthly cash flow—particularly those drawing income from withdrawals—may find SPHD the superior choice. Its predictable quarterly dividend distributions align with immediate living expenses, reducing the strain of lump-sum planning. Unlike SCHD, which defers taxable gains through reinvestment, SPHD’s quarterly distributions settle taxable events cleanly, supporting simpler budgeting.While its expense ratio is slightly higher, the difference in impact pale compared to compound growth. The convenience of direct income—coupled with SPHD’s consistent dividend arc—makes it a compelling pick for retirees prioritizing liquidity and predictability. However, SPHD’s monthly payout structure exposes retirees to potential cash flow gaps during reinvestment delays, and its slightly higher turnover introduces minor taxable events quarterly.

For those less sensitive to monthly fluctuations, SPHD’s steady rhythm offers unmatched financial clarity. In the final analysis, SCHD and SPHD represent two powerful but divergent paths to retirement income. SCHD leads where growth and efficiency dominate, rewarding long-term patience.

SPHD excels where immediate, tangible income matters most. Both reward disciplined, compound-focused investors—but only SCHD’s structural elegance and cost discipline earn it consistent top-tier status among dividend ETFs for retirement planning.

Ultimately, the decision hinges not on which ETF is objectively “best,” but on whether your retirement strategy leans toward compounding strength (SCHD) or reliable monthly cash flow (SPHD). For most long-term retirement investors, SCHD’s blend of sustainability, cost efficiency, and resilience offers the most compelling foundation for enduring income.

Related Post

The Unseen Heart Behind the Spotlight: Unveiling the Life of Lester Holt’s Wife

What Is Est Now? Unraveling the Core of a Modern Institution in a Rapidly Evolving Landscape

Blonde Male Actors Over 40: Hollywood’s Golden Boys Redefining Fame Beyond Youth

:max_bytes(150000):strip_icc():focal(959x404:961x406)/benedict-cumberbatch-sophie-hunter-62b326143ec34e0ea35e97ab26dde33d.jpg)

A Love Story Beyond The Spotlight: Sophie Hunter and Benedict Cumberbatch’s Quiet Commitment