How to Find Your Payoff Amount with Kia Finance America: A Step-by-Step Guide to Mastering Your Loan Breakdown

How to Find Your Payoff Amount with Kia Finance America: A Step-by-Step Guide to Mastering Your Loan Breakdown

For anyone who’s taken a loan through Kia Finance America—whether for vehicle financing, home loans, or personal funding—accurately knowing your payoff amount is essential. It determines your total financial commitment beyond monthly payments and shapes long-term budgeting. Understanding how to calculate this figure empowers borrowers to make informed decisions, avoid surprises, and maintain control over repayment timelines.

This guide breaks down every step, from accessing loan details to interpreting final payoff values with clarity and precision.

Why Knowing Your Payoff Amount Matters

Your payoff amount reflects the total cash required to fully settle a loan—encompassing principal, interest over time, and any closing costs. Unlike base monthly payments, which only show ongoing expense, the payoff amount reveals the complete value of the financial obligation. This data enables borrowers to: - Assess long-term affordability beyond monthly installments - Plan cash flow effectively across the loan lifecycle - Spot potential overlays like fees, points, or refinancing costs - Make data-driven decisions when renegotiating terms or considering prepayment options Kia Finance America’s transparent loan disclosures make this insight attainable—but unlocking it requires a deliberate process.

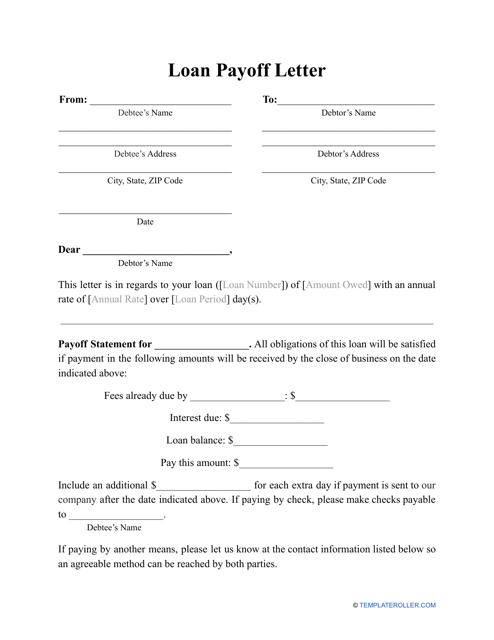

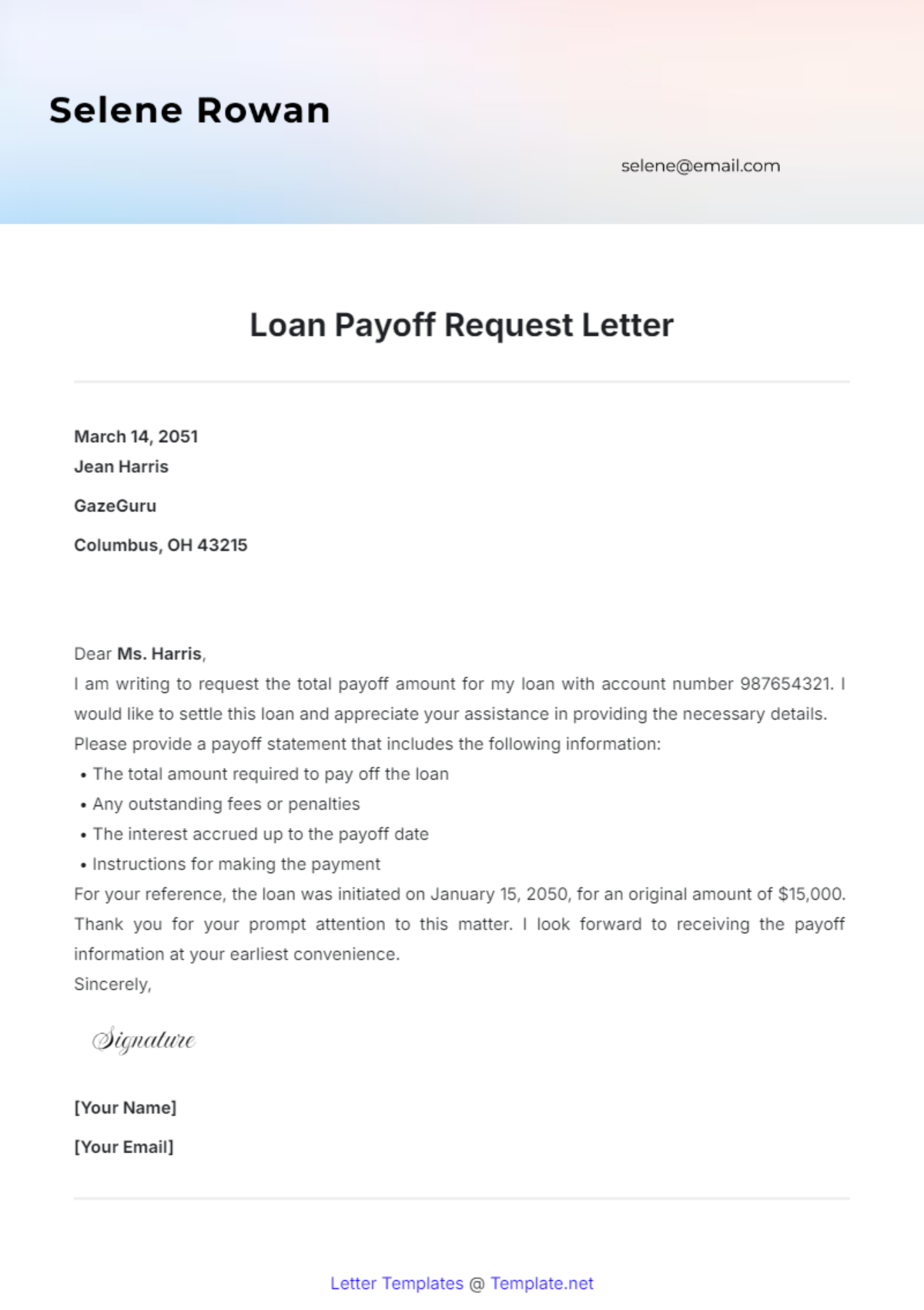

Step 1: Access Your Loan Detailed Statement or Kia Finance Portal

The first step to finding your payoff amount is retrieving comprehensive, accurate loan documentation.

Most borrowers receive an electronic statement via Kia Finance America’s secure online portal, accessible through the “My Loans” or “Account Overview” section of their official finance website. If online access is limited, contact Kia Finance America’s customer service with your account number or loan ID to retrieve a printed or digital copy. Every official statement contains critical data: - Original loan principal - Interest rate - Loan term (monthly payment duration) - Any origination fees, bridal covers, or closing costs Stringing these elements together forms the foundation for payoff calculation.

Step 2: Understand the Core Components of Payoff Amount

The payoff amount is not a single figure but a composite of principal, accrued interest, and applicable charges.

Key components include: - Principal Balance: The original loan amount borrowed. - Accrued Interest: Computing interest since the loan was disbursed, based on daily balances and periodic compounding. - Closing Costs & Fees: Some loan products include origination fees, discount points, or insurance required upfront—these subtract from principal but inflate total payoff.

For Kia Finance America loans, fees may be waived or discounted depending on credit eligibility and terms. - Closing Date Impact: Loans cleared before month-end or with weekend processing may reflect prorated balances, altering final payoff amounts slightly but staying within standard accounting principles.

Step 3: Use the Free Calculator Tool Available on Kia Finance America’s Site

For quick estimation, Kia Finance America offers an integrated payoff calculator directly on its finance portal. This tool automates complex formulas, letting users input: - Loan amount - Interest rate - Loan term (in months) - Size of any upfront fees (if known) Upon submission, the calculator returns a detailed breakdown, including the payoff amount, total interest paid, and amortization schedule.

This real-time result helps confirm official statement figures and identify discrepancies early. Users report the tool’s speed and precision as game-changing for routine financial tracking. > “The calculator removed hours of manual math,” said one satisfied borrower.

“Within seconds, I knew my final obligation—and how much interest I’d really pay.”

Without this tool, manually computing payoff requires meticulous spreadsheet modeling, which is error-prone and time-consuming. Leveraging Kia’s built-in calculator streamlines the process and boosts financial confidence.

Step 4: Calculate Manually for Deeper Insight

While calculators accelerate the process, understanding the underlying logic ensures clarity and accuracy. The standard formula for payoff amount remains: Principal × (1 + interest rate × time in years) = Total Amount Owed Breaking it down: - Convert monthly payments to annual interest using the periodic rate - Apply the standard amortization formula over the loan term - Add any non-interest fees or closing costs directly to the principal before computing total payoff Stop-motion example: A $30,000 personal loan at 7% APR over 60 months usually totals ~$33,600 in payoff—principal plus ~$3,600 in interest—requiring careful monthly interest tracking.

Kia Finance America’s loan pages often include pre-filled worksheets that rudimentarily guide this math, reinforcing understanding before formal submission.

Step 5: Account for Prepayments and Their Impact on Payoff

Borrowers who make extra payments influence their final payoff significantly. Each prepayment reduces the principal, shortening the term and cutting future interest. However, banks like Kia Finance typically apply payments to the last pin-paying installment unless pre-paid amounts are specified.

To project real-world savings: - Use amortization models to simulate reduced payoff after partial principal reduction - Factor in rebate estimates—some lenders credit full pin payments, others only partial Understanding this dynamics prevents underestimating total cost or overestimating interest savings, helping align repayment habits with true financial outcomes.

Step 6: Verify Details and Use Transparent Reporting

Once calculated, rigorously cross-check all inputs against official records. Discrepancies—such as unexpected late fees or unreported origination charges—can distort payoff accuracy. Kia Finance America emphasizes “transparent reporting,” requiring bare-minimum clutter and clear breakdowns in every statement.

Borrowers should expect: - Itemized lists of principal and interest per payment cycle - Clear definitions of fees and discounts - Visual timelines showing payoff progression This transparency builds trust and equips users to challenge inaccuracies confidently.

The True Value of Knowing Your Payoff Amount

Mastering how to find your payoff amount with Kia Finance America transforms loan management from an obligation into a strategic asset. It’s not just about numbers—it’s about empowerment. By rigorously accessing data, understanding each component, using built-in tools, and verifying outcomes, borrowers safeguard their finances and prepare for real-world repayment.

More than a metric, the payoff amount is a roadmap: one that guides smarter budgeting, informed renegotiation, and long-term financial freedom. In an era where financial literacy separates opportunity from stress, tip number one is clear—your payoff amount is in your hands. Use it wisely.

Related Post

James Brown’s Untimely Passing: The Shocking Cause Behind the Legendary Gospel Icon’s Death

Zachary La Voy Today: Shaping Public Discourse in Law, Technology, and Innovation

Louis Gossett Jr Has Two: The Unseen Legacy of a Hollywood Titan

Cat Stevens’ Quiet Love: The Enduring Presence of His Wife